Thanks for visiting our blog, where we guarantee you'll find plenty of helpful information to assist you in purchasing your new home or refinancing your current mortgage.

We also like to post technology and local interesting news.

Enjoy!

Governor Ron DeSantis issued Executive Order 20-244, moving all of Florida’s 67 counties into Phase 3.

Executive Order 20-244 does the following:

Removes state-level restrictions on businesses, such as restaurants.

Provides that no COVID-19 emergency ordinance may prevent an individual from working or operating a business, giving Floridians and business owners needed certainty and the ability to provide for themselves and their families.

Provides that restaurants may not be limited by a COVID-19 emergency order by any local government to less than 50% of their indoor capacity. If a restaurant is limited to less than 100% of its indoor capacity, such COVID-19 emergency order must satisfy the following:

Quantify the economic impact of each limitation or requirements on those restaurants; and

Explain why each limitation or requirement is necessary for public health.

Suspends all outstanding fines and penalties, and the collection of such moving forward, applied against individuals related to COVID-19.

Come one come all to The Port St. Lucie Home Show at the MidFlorida Credit Union Event Center this weekend October 3rd & 4th, 2020 from 10am to 5pm each day. The show features free admission all weekend!

At the Port St. Lucie Home Show you will find everything for your home improvement projects. View and interact with the industry’s hottest home and garden products.

Here you will find professional exhibitors with fabulous ideas for consumers. Here you’ll find the latest in products and services for home improvement. Visitors meet with professionals to make that next remodeling, renovation, landscaping or decorating project a big success. For one weekend, you’ll find wall-to-wall displays and exhibits. Most importantly you will also have the opportunity to speak directly with experts and receive advice and inspiration.

Turn your dream home or other home improvement project into a reality

Meeting your potential contractor face-to-face is the most valuable way to select professional, reliable expertise for upcoming home improvement projects. This is the perfect event for the Port St. Lucie area homeowner who is planning for the year ahead.

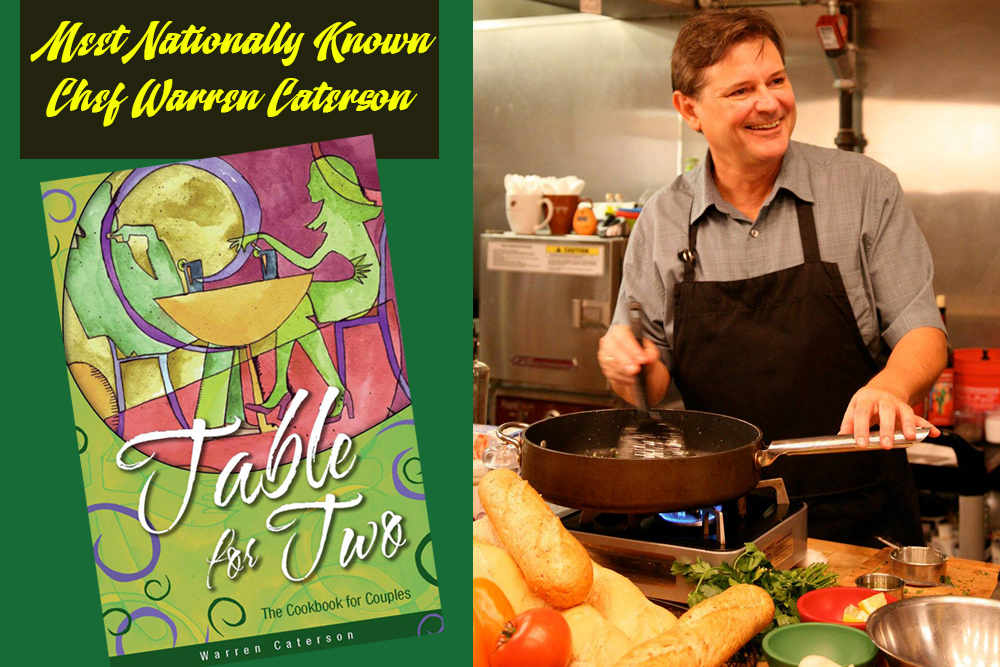

Meet Award-winning cookbook author and celebrity chef Warren Caterson at the Port St. Lucie Home Show. He will present a variety of temptingly delicious in-home culinary experiences suitable for every situation, palate, and budget.

Chef Caterson is a full-time writer and foodie. He has studied at the Southeast Institute of Culinary Arts. You too can learn how to cook healthy, using easy to find local ingredients. Chef Caterson has many creative kitchen tips to fit every budget. It makes no difference if one is cooking for two or two hundred. He is convinced that life, joy, and communion can be found in a freshly prepared and shared meal. Be sure to visit Chef Warren at the Home Show for a fun, informative experience.

MIDFLORIDA Credit Union Event Center (formerly Port St. Lucie Civic Center)

9221 SE Civic Center Place, Port St. Lucie, Florida 34952

Mortgage forbearance provided a lifeline for millions of homeowners during the difficult months of the pandemic.

But with the six-month end date for many forbearance plans rapidly approaching, homeowners will have to decide how to move forward.

Do you need to extend your COVID forbearance plan for another six months?

Or, are you ready to exit? If so, what are your options?

Here’s what you need to know if your mortgage forbearance plan is ending soon.

Millions of COVID forbearance plans are about to end

The CARES Act offered much-needed mortgage relief for U.S. homeowners.

Under the Act, if you have any mortgage backed by the federal government— including conventional, FHA, VA, and USDA loans — you can pause your mortgage payments for up to six months with no penalties.

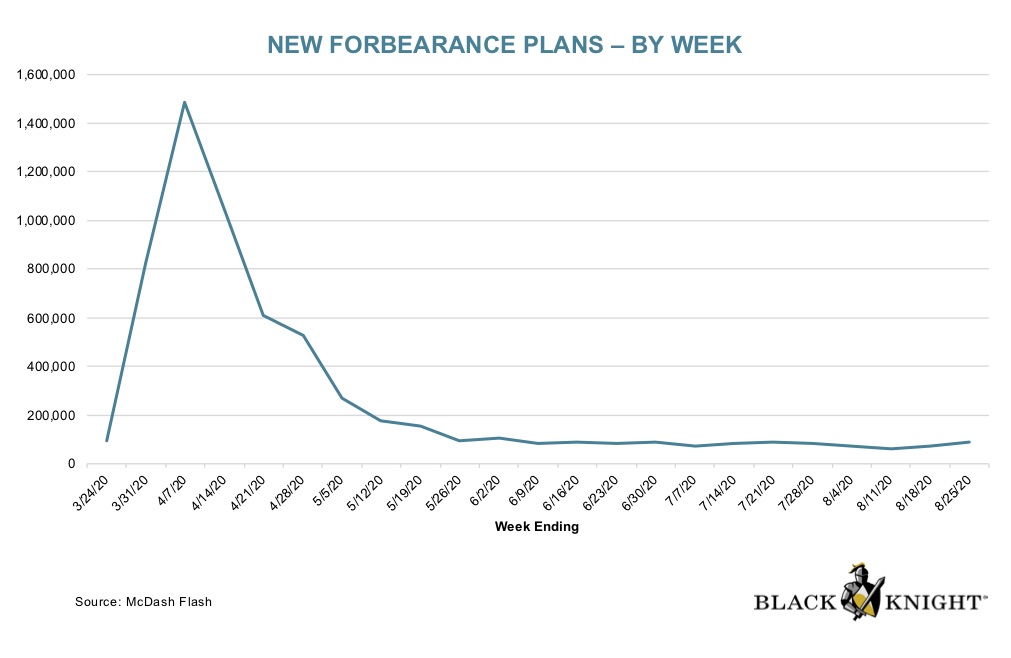

As shown in the chart below, millions of homeowners opted in for CARES Act mortgage forbearance in March and April, when the economy took its first hard hit.

Chart showing the number of new forbearance plans over time. New forbearance plans spiked in March and April, then leveled off in May through August. Source: Black Knight

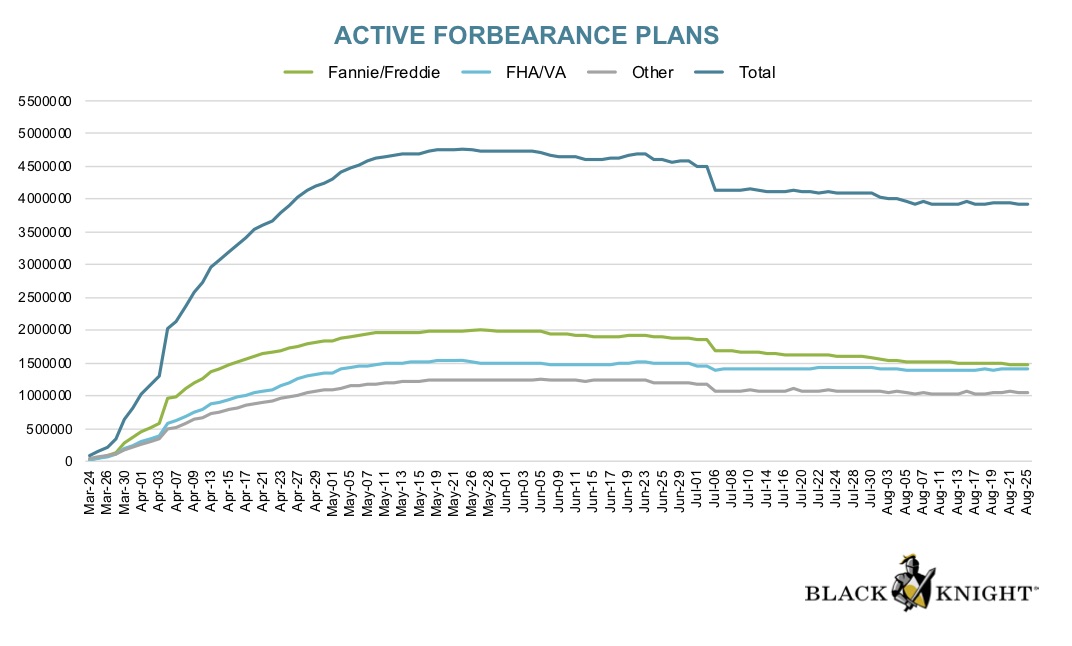

To date, the majority of homeowners who opted for mortgage relief are still in their forbearance plans.

But with the initial six month deadline nearing, many will be approaching their forbearance deadlines in September and October.

Chart showing the number of active forbearance plans for U.S. mortgages, which has hardly dropped since the initial spike in March and April. Source: Black Knight

So, what are you supposed to do if your forbearance plan is ending?

You’re free to exit forbearance if you’re able to resume making mortgage payments. If not, you might be able to extend your forbearance plan.

We’ll walk you through your options below.

Most forbearance plans can be extended for 6 more months

Six months of forbearance may have provided you a welcome buffer period to get back on solid financial ground.

But if you continue to experience money problems due to lack of employment, medical bills, or otherwise, you’re probably worried about how you’re going to pay the mortgage.

The good news? You can get a six-month extension on your loan forbearance.

That means a total mortgage forbearance period of 12 months on your government-backed loan if you need it.

Conventional, FHA, VA, and USDA loan holders can opt for another 6 months of mortgage forbearance if necessary, for a total of 12 months of mortgage relief

“From the date you seek to have forbearance, you will be entitled to that forbearance for up to one year, with an extension after the first six months of your forbearance,” explains David Shapiro, president and CEO of EquiFi Corporation.

“Forbearance plans are based on when you requested them. So if a homeowner requested forbearance in March or April at the beginning of the pandemic, September or October would be the end for the first 180 days.”

How do you request an extension?

Dongshin Kim, assistant professor of finance and real estate at Pepperdine Graziadio Business School, says your loan servicer should provide you an option to extend forbearance another 180 days if you need it.

“Loan servicers are supposed to reach out to borrowers 30 days before the forbearance plan is scheduled to end to help them understand what options they have for repayment,” says Kim.

Your loan servicer should reach out 30 days before your forbearance plan ends to discuss your options

But you shouldn’t necessarily wait for your lender or servicer to contact you about this option.

“If you need to continue your forbearance, contact your mortgage servicer well ahead of your forbearance end date,” recommends Jackie Boies, senior director of housing services at Money Management International.

“You need to prepare for relief to end now. Do not wait until you get your statement to ask a lender for help. Instead, contact them now, let them know your financial situation, and see how they can help.”

Strategies for exiting mortgage forbearance

If you are ready to exit your forbearance on time, after six months, be prepared for what happens next.

“Forbearance is not loan forgiveness. Borrowers will still owe the principal and interest that they didn’t pay during the forbearance period,” notes Kim.

“Borrowers will need to make both the regular mortgage payments and also all the payments they missed while the loan was in forbearance.”

You will typically have several options for repayment once forbearance expires:

Full repayment, which is a one-time lump sum payment. It’s possible to pay back all the missed payments at once. But lenders are NOT allowed to require this. “If you are unable to pay the lump sum, you have other options,” says Boies

Intermittent payments, where you arrange repayment with your servicer over three, six, nine, or 12 months –—whichever makes the most sense — on top of your regular payments

Lengthen your loan term and pay off the missed amount at the end of the extended loan term, with additional mortgage payments

Defer your repayment. This option lets you pay off the missed amount at the time the home is sold, refinanced, or the mortgage term ends

Pursue a loan modification. “This helps borrowers who are at risk of default change their mortgage terms – usually including a lower interest rate, reduced length of the loan, or reduced monthly payment,” adds Boies

The right option for you depends on your current finances, employment status, and ability to resume mortgage payments.

When your loan servicer contacts you, be sure to discuss every option in detail so you know exactly what to expect with the repayment plan you select.

Expect delays when contacting your mortgage servicer

The experts warn that you should anticipate a few possible snags and setbacks post-forbearance, especially when it’s time to contact your loan servicer.

“Borrowers should expect very long delays and may experience inconsistency in customer support representatives,” cautions Shapiro.

“Loan servicing organizations are not all properly staffed for the expected volume of forbearances, and they can’t train support agents fast enough to meet their needs.

“Also,” Shapiro continues, “be prepared for process changes, as regulators react to the crisis in real-time and create new rules or modify existing rules.”

Even if you can’t get through on the first few contact attempts, don’t give up.

“Be patient, but be persistent. Mortgage servicers have struggled to keep up with calls during the COVID crisis, but many have made online options easy and added staffing,” says Boies.

Keep a close eye on your credit report and score

Also, if your mortgage has been in forbearance, check your credit report carefully.

CARES Act rules state that mortgages in forbearance should not be reported as having late or missed payments. And the forbearance plan should not harm your credit score.

But this is another area where mistakes can happen.

“Sometimes there can be mistakes and issues with credit scores that can pop up around forbearance,” Kim says.

Remember, lenders and servicers have never before had to deal with mortgage forbearances on this scale. So it’s up to the borrower to be extra-vigilant and make sure nothing slips through the cracks.

Check your loan statements every month and stay on top of your credit report.

Remember, you get one free credit report per week through April 2021. So you can keep a closer eye on it than usual.

What if you still can’t afford your mortgage payments after forbearance?

The worst-case scenario: Forbearance ends and you still can’t pay your monthly mortgage. What can you do?

“You’ll probably need to consider disposition options,” says Boies.

“This may include selling your home if you can no longer afford it. Foreclosure, short sale, and deed-in-lieu are other ways of disposing of a home you can’t afford.”

Boies warns, “These options may be damaging to your credit and should be reserved until you’ve exhausted all other solutions.”

You can end forbearance early, too

You don’t have to wait for a six- or 12-month forbearance period to come to an end. Instead, you can opt to exit forbearance earlier than expected.

Just be prepared to pay back the amount you weren’t able to pay while forbearance was in place, cautions Kim.

“The best time to end forbearance is when the borrower is comfortable and able to make payments, including the additional money for repayments they owe,” Kim adds.

If you’re ready to end forbearance, contact your loan servicer and request this.

“But be sure your financial foundation is strong enough, meaning you have some type of emergency fund to backup your ability to pay your mortgage,” suggests Shapiro.

Low rates can make mortgage payments more affordable

For those exiting mortgage forbearance in the next few months, there may be an opportunity to lower your mortgage payments below pre-pandemic levels.

Rates have hit record lows nine times in 2020, and are set to remain low for months — if not years — to come.

Some options for exiting mortgage forbearance would allow homeowners to secure a new, lower rate and make their monthly payments more manageable.

Ask your servicer about loan modification and refinancing.

If these options are available to you, you might be able to exit forbearance much more confidently, knowing that you’ll have a more affordable mortgage payment on the other side.

Finnish research has discovered the functional ability of older people is much better today, compared to people of the same age three decades ago.

This finding was observed in a study conducted at the Faculty of Sport and Health Sciences at the University of Jyväskylä.

The study compared the physical and cognitive performance of Finnish people between the ages of 75 and 80 nowadays with those of people the same age in the 1990s.

“Performance-based measurements describe how older people manage in their daily life, and at the same time, the measurements reflect one’s functional age,” says the principal investigator of the study, Professor Taina Rantanen, in a statement.

Among men and women between the ages of 75 and 80, muscle strength, walking speed, reaction speed, verbal fluency, reasoning and working memory are nowadays significantly better than they were in people at the same age born earlier. In lung function tests, however, differences between cohorts were not observed.

“Higher physical activity and increased body size explained the better walking speed and muscle strength among the later-born cohort,” says doctoral student Kaisa Koivunen, “whereas the most important underlying factor behind the cohort differences in cognitive performance was longer education.”

Postdoctoral researcher Matti Munukka continues, “The cohort of 75- and 80-year-olds born later has grown up and lived in a different world than did their counterparts born three decades ago. There have been many favorable changes.

“These include better nutrition and hygiene, improvements in health care and the school system, better accessibility to education and improved working life.”

The results suggest that increased life expectancy is accompanied by an increased number of years lived with good functional ability in later life. The observation can be explained by slower rate-of-change with increasing age, a higher lifetime maximum in physical performance, or a combination of the two.

“This research is unique because there are only a few studies in the world that have compared performance-based maximum measures between people of the same age in different historical times,” says Rantanen.

“The results suggest that our understanding of older age is old-fashioned. From an aging researcher’s point of view, more years are added to midlife, and not so much to the utmost end of life. That’s hopeful news for us all.

The nation’s largest “WaveGarden,” a simulated surfing park, is slated to come to Midway Road as a part of a 200-acre community development.

It is to feature 800 residential homes, 600 hotel rooms, 400,000 square-feet of retail space, 125,000 of office space and thousands of potential jobs.

The new “Willow Lakes” village is expected to cost $595 million in new construction, according to the developers, and the first phase of building could begin in the third quarter of 2021, depending on permitting and approvals.

The first phase, to run $40 million, would feature the WaveGarden and food and beverage facilities. It may also include a 150-room hotel, according to the project manager. The surfing center itself, “Surfworks Resorts” is expected to create 139 jobs and $15.6 million economic impact annually, according to a study by the Economic Development Council of St. Lucie County.

The project is expected to create about 3,400 jobs during construction and nearly 1,900 jobs annually, according to the Economic Development Council.

City commissioners unanimously approved a first set of sweeping zoning changes to begin to clear the way for the Willow Lakes development, which is near Interstate 95.

“This is probably one of the biggest things that could happen to us,” Commissioner Thomas Perona said.

The developers have owned the land at 10050 West Midway Road since 2004. They were looking for a “destination” project, but were slowed down by the Great Recession. They found something they liked with the WaveGarden, Willow Lakes Manager Chad Labonte said.

“The last thing we wanted to do was another golf course community,” Labonte said. “This is a game changer.”

There are a handful of WaveGardens around the world, but dozens in the development stage, Labonte said. This would be the largest. A similar Surfworks Resorts is planned in Myrtle Beach, S.C.

The facility features a massive swimming pool-like area that creates up to 1,000 waves an hour and around 100 surfers at any moment, according to a promotional video the developers showed. Waves are of varying shapes and for a range of expertise.

“It will attract people from Fort Pierce, across the country and around the world,” W. Lee Dobbins, attorney for the Fort Pierce firm Dean, Mead, Minton, Zwemer, said.

The bold proposition is expected to generate $8.7 million in impact fees, not including the WaveGarden itself and a proposed TopGolf, according to city documents.

Willow Lakes is designed to be its own community.

Projects range on the number of homes that will be built, which is in part dependent on how dense the city allows for the developer to build. City documents submitted by the developer suggest up to 1,000 residential buildings, 700 of them are to be multi-family homes, 150 single-family townhouses and 150 single-family detached homes.

The project has gone through traffic studies, engineering reviews and environmental concerns.

“It’s really planned as a whole new coastal community, which is several miles away from the coast,” Geoff Fitzgerald, land planner with Bohler, said. “It’s planned around a WaveGarden.”

Commissioners offered glowing endorsements of the plan, excited for a developer building a unique project in Fort Pierce.

Backing the project was Pete Tesch, president of the St. Lucie County Economic Development Council. He suggested it would be a big economic boon for the local economy.

“Willow Lakes and the surf park project in our view is a catalytic economic development event which has the ability to ‘move the needle’ on our collective efforts to enhance Fort Pierce’s reputation as a premier tourist destination and further diversify our growing economy,” Tesch wrote in an endorsement letter to the commission. “As we enter the ‘new normal’ and the post COVID-19 environment, this important project will have a historically significant impact on our community.”

Due to the coronavirus, many schools are out or transitioning to distance learning and we understand your kids are home with you or other in-home caregivers. Use our free activities to help children build the important skills they will need to manage money into adulthood.

With children unexpectedly home from school–from preschool through college–you may be looking for ways to keep your kids engaged and learning. We have created games and activities that can help your children and young adults gain money skills. Best of all, you don’t need to be a money expert to use them. Here are some tips and activities to help you teach your kids about personal finances.

To build money skills, follow the three building blocks

We have conducted research on how children and young adults develop the financial capability that they’ll need in adulthood. We break this down into three “building blocks” that children acquire as they grow. All our financial education activities are based on these three building blocks:

Executive function

The ability to plan ahead, remember information, multitask, solve problems, and control impulses. Children develop these abilities as early as age 3 and continue building them throughout childhood.

Financial habits and values

People use standards, shortcuts, routine practices, and rules to live by, in navigating daily financial activities. These areas develop quickly during elementary school and in the preteen years.

Financial decision-making skills

It is important to build familiarity with financial concepts and competency in research and analysis. Teenagers and young adults have good opportunities to develop these skills.

Using the building blocks as a framework can help you keep your conversations about money age-appropriate. If your children have questions about money topics, you can keep the building blocks in mind when you answer. For example, if your child asks about credit cards, here’s how you might answer:

For a young child, emphasize planning ahead

“Buying something with a credit card might not look like I’m spending money, but I am. I’m making a promise to pay my credit card bill later, and I have to keep my promise.”

For a school-age child, connect to your values

“Credit cards are convenient, and it’s important to use them wisely. My personal rule is to use cash for anything under $20, to make sure small things don’t add up to a big credit card bill.”

For a teenager, build research skills

“Let’s find an online calculator to see how much it costs to pay off a $1,000 credit card bill by paying the minimum balance each month.”

Free financial education activities for parents to use with their kids

We’ve compiled some of our Money As You Grow and Youth Financial Education classroom activities for you to use with your kids. To use the classroom activities, you may want to read or download the teacher guide yourself, and then print the student guide and activities for your child or allow them to complete the worksheets digitally.

Preschool (ages 3 to 5): Build money foundations

Children ages 3 to 5 are usually too young to understand abstract financial concepts, but they can build a foundation to serve them well in the future. These resources help your child with executive function – the ability to plan ahead, delay gratification, multitask, solve problems, resist impulses, and more.

Play pretend – Pretending helps children focus, think flexibly, and plan ahead. Use the scenarios in the activity or use your own imagination! Download the pretend play activity.

Space Journey Choices – In this activity, your child decides what to bring on a tiny rocket ship. Help them practice making choices and tradeoffs with limited resources, a key part of money management. Download the space journey activity.

Money as You Grow Bookshelf – Read some of these popular children’s books and use our parent guides to help talk through the money lessons. Note: If you don’t have the books, you can still use the activities on the last pages of the guides. See the books that are part of the Bookshelf.

Active games that build self-control – These help children learn how to wait, follow directions, pay attention, and practice controlling their behavior. Examples: Follow the Leader, Simon Says, and Red Light Green Light.

School-age children (ages 6-12): Absorb financial habits and rules of thumb

Between the ages of 6 and 12, you can help children absorb guidelines and day-to-day habits that shape how they earn, save, and shop. Help your school-age child or preteen develop financial habits and values. Keep in mind that discussing these activities with your child – as they go, or afterward – can help them process and use what they’re learning.

Bingo on the go – While practicing physical distancing, drive or walk around your community and check off different types of places around your home and talk about how each place is funded – public, private, nonprofit, or a combination of these. Download the bingo activity.

Using idioms to promote saving – Every language has wise sayings or phrases that offer advice on how to live responsibly and thoughtfully. In this activity, your child can explore English expressions that use figurative speech to better understand financial concepts like saving and earning. Download the money expressions activity.

Building a good borrowing reputation – People with a good reputation as a borrower are more likely to earn the trust of a lender. In this activity, your child analyzes the profiles of three different people to decide what kind of borrowing reputation they have. Download the borrowing reputation activity.

Test the claims of a TV commercial – Explain to your child that TV commercials use special words, music, and settings to make us want to buy. In our bookshelf parent guide for “Bargain for Frances,” it discusses an activity to help your child realize how commercials can impact our thinking. We can be disappointed if we buy something advertised without checking it out first. Download the parent guide, page 9 has the commercial activity.

Money As You Grow Bookshelf Parent Guides – Even if your child has outgrown the books, you can still download the Parent Guides and turn to the last pages for activities to do around the house. Visit Money As You Grow Bookshelf.

Teens and young adults (ages 13 to 18): Research and practice making money decisions

Teens and young adults generally start to earn money and make decisions on their own. Adult supervision, guidance, and feedback can help them navigate successfully. Below you’ll find some selected activities for your teenager or young adult that help with financial knowledge and decision-making – the research and comparison shopping skills that help them find trustworthy information, process it, and apply it to their own situation. Keep in mind that discussing money decisions with a trusted adult can help teens gain confidence in their own reasoning.

Family members’ jobs – With this activity, your teen can reach out to family members to research and compare the jobs they hold and what education and training it took to get there. Download the family jobs activity.

Reading about insurance – Insurance helps protect people from health and financial risks. In this activity, your teen learns ways to protect themselves from risk and avoid high costs when something goes wrong. Download the reading about insurance activity.

Choosing the best cell phone plan for you – Product research and comparison shopping help people make informed buying decisions. Your teenager can research the features and costs of cell phones and cell phone plans and use a decision matrix to compare options. Download the cell phone plan choice activity.

Reporting fraud and identity theft to authorities – Fraud and identity theft hurt millions of Americans every year. In this activity, your teen matches fraud and identity theft crime descriptions with appropriate action steps to take in the event of a real-life crime. Download the fraud and identity theft reporting activity.

FDIC Money Smart

Check out these resources from our partners at the FDIC! They have activities, lessons, and ideas to help children strengthen money habits and values.

Thousands of people, along with me, are surely missing the local neighborhood dive bar.

The ‘come as you are’, no-judgement pub covered with beer insignias is a vibe that you just can’t get anywhere else.

But, if you’ve ever wanted to recreate that feeling at home, now is your chance. Miller High Life is giving away a backyard dive bar valued at $10,000 to one lucky fan.

But the contest closes on September 22, 2020.

The glorified shed, where you’ll always be “a regular”, comes with:

Sticky floors, duh

An actual bar with Miller High Life tap handles

Quirky bar stools

A popcorn machine

A spot for a bouncer if your neighbors try to crash your bar

All the wood paneling you could ever want

The dimmest of lighting

Quirky beer artwork

Doors that open completely to allow for patio season

Enough beer to live the high life from your own yard for the rest of the year

“All of this from the comfort of your own yard!” touts Miller in a press release.

To enter the Backyard Dive Bar giveaway, you have to be 21+ years old. Just text “DIVEBAR” to 90464 to receive a link for the simple entry form. Or, you can enter by visiting www.HighLifeDiveBar.com.

Nothing but your basic contact info is required. The contest closes tomorrow September 22nd and winners will be announced shortly thereafter.

Two-thirds of Americans said quarantine has made them a better person, according to a new survey.

The poll of 2,000 Americans over age 21 looked at the positives changes to come from this challenging time—and the ways in which respondents are re-prioritizing what they value.

Results revealed 55% of respondents were a bit embarrassed by some of the things they valued pre-quarantine, and the many months spent at home gave 70% a chance to learn more about themselves.

Commissioned by Coravin and conducted by OnePoll, the survey found that the quarantine has, understandably, changed Americans’ outlook on life.

Some respondents gained the time and flexibility to delve into new hobbies and discover new passions— shortages of baking products in the grocery store was proof of this. And, 35% said they want to continue those hobbies once quarantine is over.

This opportunity to explore personal interests beyond work has led 27% of respondents to indicate they are hoping to achieve a better work/life balance coming out of quarantine.

Being close to the people we care about was a major theme for respondents, as 46% want to spend more quality time with friends and family, and 38% plan to create more meaningful relationships with those around them.

TOP THINGS PEOPLE NO LONGER TAKE FOR GRANTED:

Spending quality time in person with family or friends 52.28%

Hugs 41.23%

Traveling to new destinations 32.53%

A relaxing walk in the park 31.99%

Shopping in a store 31.73%

A date night at a restaurant 31.39%

Extended family gatherings 30.86%

Attending events in person 28.92%

Stopping for a cup of coffee on my way to work 25.90%

Meeting new people 25.70%

Weekly coffee dates with friends 24.36

Post-work happy hour 23.69%

Chatting with co-workers during lunch 23.56%

Having a quiet weekend at home be out of the ordinary 22.96%

An afternoon at the beach 22.36%

Sending my children off to school in the morning 21.49%

Attending sporting events 21.22%

Wandering through a bookstore 20.68%

Watching my kids’ sporting events 18.14%

Hitting the gym 17.54%

Dropping my kids off at playdates 16.06%

THINGS PEOPLE WANT TO DO AFTER LOCKDOWN SELF-REFLECTION:

Spend more quality time with friends and family 45.60%

Work to create more meaningful relationships with loved ones 37.70%

Continue new hobbies I started during quarantine 34.80%

Attend in-person events after attending their virtual counterparts during quarantine 29.40%

Move to be closer to loved ones 27.90%

Focus on achieving better work/life balance 26.60%

Change careers in order to have more meaningful work 21.80%

Project Evergreen has been mowing lawns for frontline workers taking some of the stress out of their lives while beautifying the environment for when they return home.

During the pandemic, households with a first responder or healthcare worker do not need to be thinking about getting their yard work done. That’s why the national non-profit, which is fueled by volunteers from landscaping companies like Weed Man, show up at the homes of essential workers like Logan Gillen, an ER nurse, who can then spend hours with his family when he’s not at work.

The project pairs Weed Man franchisees with local heroes near them, providing free services to help 38 healthcare workers. So far, the project has delivered manicured lawns to front line heroes in six states. Other volunteers, like church groups, have been paired with heroes as well.

“The Green Care Program for front line workers has given us at Weed Man Fresno an opportunity to show our appreciation and help those who dedicate their lives to helping others,” said owner Jeff Kollenkark.

“We have a total of nine customers in the program and are blessed to be able to give back to the hard working front line workers who put their lives at risk every day.”

Cindy Code of Project Evergreen said volunteers at nine locations in seven states have been servicing military families through the GreenCare for Troops program since 2006.

Military families face many challenges when their love one is deployed, and taking lawn care off their to-do list has been a big help—and in 2020 they expanded the initiative when they saw the hospital workers feeling the same stress.

Trimming some of their workload by trimming their grass has proven to be a great way to show our heroes some ‘corona kindness’.

Instruments come in all shapes and sizes, but a company called Playtron has created a MIDI device that allows you to play fruits and vegetables.

While this seems ridiculous, a YouTuber called MEZERG created a viral electronica song and corresponding music video called “Watermelon,” in which, you guessed it, he plays slices of watermelon like Stevie Wonder played his synthesizer on “Superstitious.”

The device, called a Playtronica, works on smartphones and tablets provided you have the correct adaptor and a music application such as GarageBand.

It’s compatible with most synths and musical gadgets with a USB MIDI input.

Simply connect cables to your fruits and veggies, and complete the circuit by touching the ground wire with one hand and note wire with another.

So sit back, click play and enjoy watching “Watermelon” below to see MEZERG taking playing with one’s food to a whole new level.

Millennials are getting handier around the home since COVID-19 lockdown measures began, according to this new survey.

In fact, the poll of 2,000 homeowners found that compared to other generations, millennials have been the busiest, with 81% having tackled a home improvement project since March.

Conducted by OnePoll in conjunction with blow torch manufacturer Bernzomatic, the survey examined the various home improvement projects that American homeowners have completed while stay-at-home orders have been in effect—and why they chose to take them on in the first place.

Two-thirds of the respondents say they tackled their project to save money while 49% simply needed something to keep themselves busy during lockdown.

Overall, the average homeowner has attempted four different home improvement projects since March and saved an estimated $160 simply by attempting to complete a project themselves.

From painting the house (32%) and working on landscaping projects outside (29%) to re-caulking (27%) and re-tiling kitchens and bathrooms (24%), homeowners have kept themselves busy these past six months.

Not only have these projects kept homeowners busy, they have also led to new hobbies; 73% of those who tackled a home improvement project on their own revealed that afterward, they felt resilient enough to keep taking on more projects and 67% of homeowners look forward to tackling more projects in the future.

And there’s more to be done, as 71% of homeowners still said their home is a “work in progress.”

It’s no wonder that half of the homeowners surveyed (50%) plan on doing a DIY home improvement project before the end of this year.

Twenty-nine percent plan to work on landscaping projects outside, while 57% plan on taking on projects ahead of the holiday season.

Holiday-prep projects include bathroom and kitchen renovation, filling driveway cracks, fixing the patio landscape and replacing countertops and kitchen floors.

10 HOME IMPROVEMENT PROJECTS AMERICANS LOOK FORWARD TO CREATING FOR THE HOLIDAYS

After the world’s largest landfill closed down, New York State officials and nonprofits facilitated a decades-long transition from dump to green outdoors space.

Creating a park three times the size of Central Park? That’s not so easy. The conversion has involved goats, using landfill fumes to methane-power homes, and plenty of manpower as buried trash gets turned into rolling hills of native grass.

Fresh Kills landfill, once the dumping site for all of New York City’s garbage, was a place that once terrorized Staten Islanders with odors and the sight of trash mounds said to have reached 20 stories high.

Now it’s just months away from reopening as one of the world’s great rewilding projects in the boundaries of one of the most densely populated areas in the Western Hemisphere.

Originally promised as a park by former mayor Michael Bloomberg during a dip in the polls, the dump closed in 2001, allowing sanitation department officials to begin work to control the pollution.

The desire to turn it into a park led the Department of City Planning to host an international design competition—the project for creating New York City’s largest park construction in over a century eventually went to the Field Operations firm.

Trucks of iron-rich soil were brought in from New Jersey to cover plastic sheeting that “capped” the garbage mounds, staining local roads red, while methane extraction pipes channeled the fumes of the underground detritus into Staten Island homes to power heating and stoves.

Next, concrete troughs were constructed to funnel rainwater quickly away from the trash hills, and a local park was restored, along with the baseball diamond, handball courts, and playgrounds. Goats were brought in for their ecological restoration abilities in 2012.

Centered around four capped garbage mounds, fields of native grass species sparkle and wave under the sun, and trails through sun-dappled groves give habitat to mid-Atlantic birds like the grasshopper sparrow.

The mounds are separated by tidal creeks and natural waterways which recapture the image of the Dutch word (kille) for tidal marsh and wetlands that gave the area its curious name “Freshkills” back in 1930.

Turning the world’s largest landfill, once home to 150 million tons of trash, into a 2,200 acre state park takes time. The plan is for Freshkills to open in stages, starting with the North Park Phase 1, in which 21 acres will open to the public next spring, and continuing incrementally for another decade and a half.

The Freshkills website features some 360° pictures that allow you to understand not only the scope of the park, but a chance to imagine what was there before.

The ultimate image of renewal, Freshkills social media pages take advantage of the triumph of all parties involved to educate people on the importance of wetlands, grasslands, animals, and outdoor recreation—all things which New Yorkers will be overjoyed to experience in earnest once the lockdowns lift.

…And where those rules about white after the holiday came from, while we’re at it.

Labor Day is one of the least recognized, forgotten-about-until-around-the-corner holidays of the year—one that we seem to appreciate only after realizing it affords us a three-day weekend come September. Here, seven tidbits you probably never knew about the holiday.

The first Labor Day celebration was September 5, 1882 in New York City.

On that Tuesday, 10,000 citizens marched for labor rights down the streets of Manhattan. During this time the average American worked 12 hours a day, six days a week. It wasn’t until the Adamson Act passed on September 3, 1916 that our modern eight-hour work day was established.

The holiday is often confused with “May Day.”

Most other countries celebrate International Workers’ Day, or “May Day,” instead of Labor Day. The concept is the same, but it is celebrated on May 1 around the globe.

The theory about why we can’t wear white after Labor Day is highly debated.

There are three hypotheses about the origins of the “no white after Labor Day” directive. The first theory, disagreed upon by many, is based on class distinction in the early 1900s. Although white clothing was clearly an upper class luxury, after the Civil War it became harder to distinguish women coming from old money or new money. The higher class ladies then made inane fashion rules to weed out those who were “out of place.”

The second theory speaks to a more practical approach by pointing out that Memorial Day and Labor Day bracketed the summer season, and therefore lighter, summery, white clothes were no longer needed.

The last theory has to do with popular fashion magazines, who may have begun promoting fall clothing after Labor Day, and the trend was picked up.

Whatever the reason may be, it’s safe to say the fashion rule is kaput.

Labor Day ironically causes some of the longest working hours for retail workers.

Labor Day weekend is notorious for having crazy sales. But unfortunately, this means retail workers (a faction that makes up 6% of the country’s employment system) have to work longer hours on a day specially dedicated to labor appreciation. In fact, many other professionals are expected to work on Labor Day as well including correctional officers, police officials, firefighters, nurses, and more.

It is the second most dangerous holiday weekend to drive on U.S. highways.

According to CBS News, there were 308 casualties over Labor Day weekend between 2011 to 2015, following closely behind Memorial Day’s 312 casualties. These particular holidays designate the beginning and ending of summer, where excitement is heightened and young people tend to be more reckless on the road.

The holiday also symbolizes other endings and beginnings.

Yes, Labor Day is the “unofficial end of summer” and the end of hot dog season. But it is also the beginning of NFL season—almost every NFL kick off game has started the weekend after Labor Day. Labor Day is the end of white pants but the beginning of black pants… and it’s also, unfortunately, the end of three day weekends until November.

In a week’s time, the United States’ oldest living American to have served in the Second World War is going to turn the grand old age of 111.

To help him celebrate, the National World War II Museum is asking people from all around the world to send him a birthday greeting.

So what is life like for a 110-year-old? If you’re Lawrence Brooks—who in the early 1940s was stationed in the Pacific as part of the 91st Engineer Battalion—you spend lots of time doting on your five children and five stepchildren, your 12 grandkids, and an incredible 23 great grandchildren.

If you’re Lawrence, you also love celebrating your big day with others at the National World War II Museum in New Orleans.

On those jubilant occasions, there’s live music. There’s cupcakes. It’s a fun day for all.

But because of the pandemic, on his birthday this year Lawrence won’t be able to celebrate with lots of others.

Luckily, the museum has come up with a novel idea for Lawrence’s September 12 birthday this year: Well-wishers can send the supercentenarian a birthday card the old-fashioned way: by mail.

Lawrence, who lives with his daughter in New Orleans’ Central City neighborhood, reflected on his long and interesting life to National Geographic. And he gave a few words of wisdom. Eat right. Stay healthy. Most importantly? ”Be nice to people.”

Now you know a little of Mr. Brooks’ story, perhaps it’s time to find that stash of letter paper, your fanciest pen, and celebrate by sending the veteran a card?

Here’s the mailing address you can send your birthday greeting to:

The National WWII Museum

c/o Happy 111th Mr. Brooks!

945 Magazine St.

New Orleans, LA 70130

Happy writing! And be sure to check out the National World War II Museum’s social media on September 12 for a special birthday video.

A dedicated wildlife photographer has spent three years amassing a stunning collection of images of the UK’s most beautiful butterfly species—some of which he took right from his backyard during lockdown.

Andrew Fusek Peters has captured the series of colorful shots after studying the behavior of butterflies in the British countryside since 2017.

Incredible photographs show 17 different species of the winged insects in full flight or taking off from flowers across Worcestershire and Shropshire.

Andrew says he took over 150,000 frames to achieve his unique collection of images and believes he is the first person to shoot such a variety of butterfly species.

His photos include everything from the painted lady, green hairstreak, marbled white, silver studded bleu, and red admiral, to the dark green fritiallary and Essex skipper butterflies.

The 54-year-old from Lydbury North said, “I’ve spent three years studying the behavior of UK butterflies and working to capture them in motion. It was worth the effort to show their incredible delicacy and beauty in flight… quite a lot during lockdown were in my garden.

“I’m using a very high speed camera to shoot the butterfly in flight and it also requires understanding and knowledge of when the butterfly is going to take off.

“There are very few shots like these in the world because there are very few people who can capture a butterfly in focus as it takes off from a flower.

“I shoot at 50 frames per second and I haven’t got them in a studio. I’m out in the wild and I’m able to get up close and personal.

“My favourite is the Brimstone because of its beautiful, buttery colour. They say the word butterfly from Old English comes from the color of the Brimstone.

In my image, “you can actually see the shadow of the proboscis, which it uses to drink nectar from a flower. It is extraordinarily clear.

“The wood white is quite rare and an extraordinary color and beautiful in flight.

“The clouded yellow is fairly rare and flies over from Europe, but what’s super rare is to get them all in flight.

“My next big project will be to take flight shots of every single one of the UK’s butterfly species. I’ve set myself a mad challenge as there’s been 71 recorded in Britain.

“I think that will take another five years and require a lot more travel across the entire country.”

Have you ever tested your photography skills on flying butterflies? Get some tips by looking at Andrew’s excellent images below.

An easy way to tell a butterfly from a moth? Only butterfly antenna are shaped like clubs, with a bulb at the end of a long shaft.

Lavender is one of the herbs many butterflies love.

Butterfly? Or tiny leaves falling through the sky?

Butterflies may come in many different colors, but they all evolved from the same common ancestor over 225 million years ago.

Can you see the shadow of this brimstone’s proboscis?

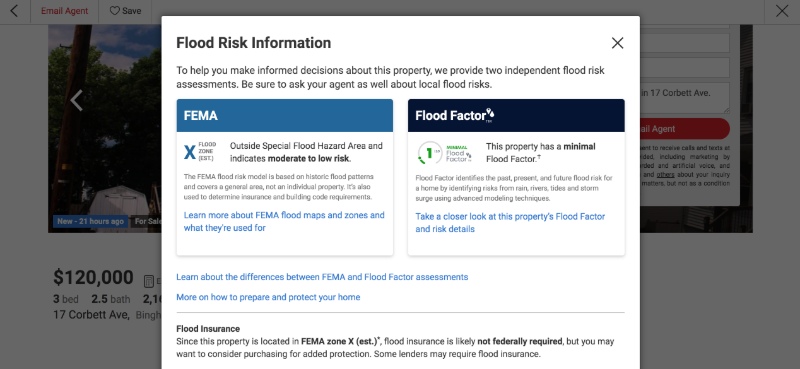

Since buying a home will be the most significant financial decision of most people’s lives, prospective buyers deserve to understand the full cost of their investment. That’s why a nonprofit, First Street Foundation, is compiling an updated list of the flood-insurance risks for millions more properties nationwide and publishing their findings online for all to see.

As changing climatic conditions have resulted in storms of greater strength and in greater numbers, the nonprofit group is filling in the massive gaps in the Federal Emergency Management Agency (FEMA) flood zone designations.

“Unfortunately, inaccurate FEMA flood maps and nonexistent or weak real estate disclosure laws make it extremely difficult for home buyers to learn of a property’s flood risk or even its flood history,” Joel Scata who studies flood risk at the Natural Resources Defense Council, told NPR.

FEMA has around nine million properties in flooding zones, wherein homeowners would be required or advised to buy flood insurance, however First Street Foundation’s clever combination of data has produced a more accurate flood risk map that takes into account climate change, sea level rise, and altered rainfall patterns and storm paths, and that will continue to update faster and more efficiently than FEMA’s flooding maps.

Through the unprecedented partnership of more than 80 world-renowned scientists, technologists, and analysts working together, First Street was able to identify an additional 14.5 million homes that are in potential flood areas.

Their tool, Flood Factor, allows you to enter a zip code and bring up anything that’s available on homes in that area.

However, the effort has been looked at glumly by major real estate companies and homeowners alike who are worried that flood risk designations would diminish the property value of their homes

But Realtor.com agrees that buyers deserve to know everything, risks included, about a home before making a purchase, and now all 110 million listed properties on their website contain either publicly or privately assembled flooding data.

“They can elevate their home on stilts. They can add a sump pump into the basement. They can install a rain garden outside,” Realtor.com executive Leslie Jordan told NPR. “But they must know their risk first.”

Welcome to the online application for St. Lucie CARES. This program will provide a one-time payment to eligible St. Lucie County residents who have suffered an economic hardship due to the COVID-19 pandemic. The program is designed to help with payments for the following: rent or mortgage, homeowners association dues, utility bills, homeowners/flood insurance bills, auto loans, and car insurance. Documentation required for the program can be uploaded directly to the online application.

Read the information below, and please apply if you meet the criteria.

Click here to download the full document for more information on CARES Funding for St. Lucie County.

Who is eligible for St Lucie CARES?

Any St. Lucie County resident who has suffered an economic hardship (i.e. a reduction or loss of employment income) caused directly by COVID-19, and who earns less than 120% of the area median income (as shown in the table below) is eligible to apply. All household members should be listed on your application.

Household Size

1

2

3

4

5

6

Income Level

$58,440

$66,720

$75,120

$83,400

$90,120

$96,840

What can the assistance pay for?

Funding from the program is allowed to be spent on the following household expenses. Payments must have been due after March 1, 2020. Payments due prior to this date are not eligible.

Applicants are eligible for a onetime payment of up to $4,000. The actual amount of assistance received per household will be determined on a case by case basis.

What documents do I need to apply for St. Lucie CARES assistance?

Government Issued Picture ID’s (all adults over 18 years old);

Child Verification: Birth Certificates or SS card, or shot records or school ID (only for children). Only one form is required;

You will be required to provide documentation of the expenses you are requesting assistance with. They must be in the name of a household member and the name must be referenced on the bill.

Rent: a signed and dated rental notice from the landlord stating the amount due. The notice must include the name and contact information of your landlord.

Mortgage: a copy of your most recent mortgage statement.

Utilities: statements for FPL, FPUA, St. Lucie County utilities, or Port Saint Lucie Utilities,

Homeowner Association Fees: billing statement

Homeowners/Flood Insurance: billing statement

Car Payment: billingstatement

Car Insurance: billing statement

What happens next?

After you submit your application you will receive an email confirmation. An intake specialist will contact you within as soon as possible to review any additional documentation that may be needed.Please understand additional information may be requested and required after your application has been reviewed. You will have an opportunity to work with an intake specialist to provide any additional information. We will ask you to provide documentation within 72 hours of speaking with your intake specialist. We appreciate your patience as we help your household recover from COVID-19.

If I’m approved for assistance, how long will it take to receive my payment?

Once you have been notified that you have been approved for the program, payment should be processed within three weeks. In order to provide you with your payment as quickly as possible, you will be required to sign up for direct deposit.

Approved applicants will be required to complete an IRS W9 form for federal income tax purposes. Funding from this program is taxable and must be reported to the IRS. You will receive an IRS 1099 form at the end of the year.

If you need assistance to complete the online application, please contact the CARES Public Information Line at (772) 462-1705 Monday – Friday 8am – 5pm, or emailcomm_info@stlucieco.org.